In this article, we wish to remind you of some major changes that will come with the implementation of ANC Regulation no. 2022-06, whose application is mandatory for all financial years beginning on or after 1 January 2025.

I. The new definition of exceptional items

Exceptional items must now be linked directly to a major and unusual event:

- A major event is one where its consequences are likely to have an influence on the judgement of users. Income and expense items linked to a major and unusual event are those that would not have been recognised in the absence of that event.

- An unusual event is one that is not related to the entity’s ordinary course of business;

Appreciation of what constitutes a major and unusual event is specific to each entity.

This means that normal and routine operations that are part of the ordinary course of business are now excluded from the exceptional items and are recognised in operating income/loss (résultat courant) according to their nature, in net income/loss from operations or in financial income/loss.

- Examples of normal and routine activities: Disposal of a fixed asset, disputes, penalties paid or received on purchases and sales, production stoppages, consequences social contributions and tax audits, impairment of equity securities held in subsidiaries.

- Examples of major or unusual events: a withdrawal or divestment (e.g. abandonment of activities or assets that are no longer connected to the entity’s normal and routine activity), an expropriation, a cyberattack, a natural disaster. These are the type of events liable to meet the conditions.

Remaining items necessarily included in exceptional items:

- accounting entries that are purely tax-based (accelerated depreciation, etc.)

- changes in accounting methods

- corrections of errors

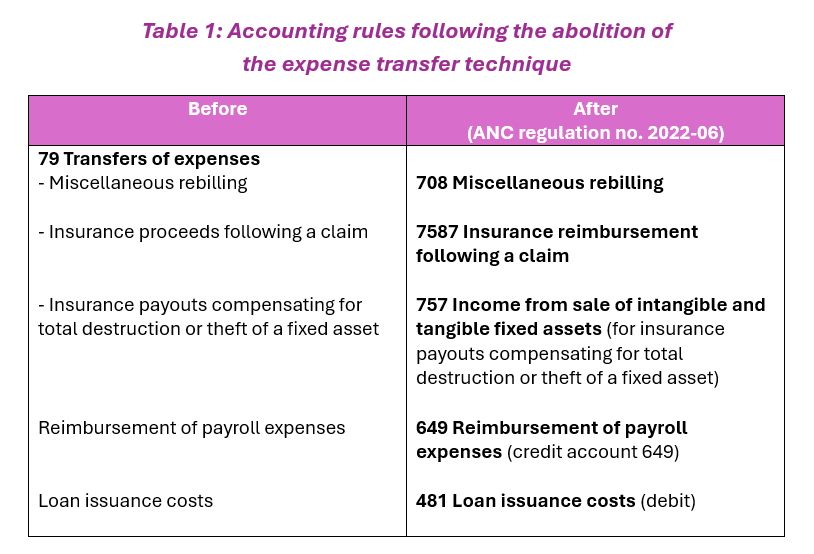

II. The abolition of the expense transfer technique (79xx accounts)

The regulation abolishes the use of the expense transfer technique: accounts 791, 796, 797 must no longer be used.

The ANC proposes new accounting rules for the cases concerned, such as:

- Allocation of loan issue costs over the term of the loan when these costs are capitalised;

- Rebilling of staff costs;

- Reimbursements received directly as compensation for staff costs;

- Insurance settlements.

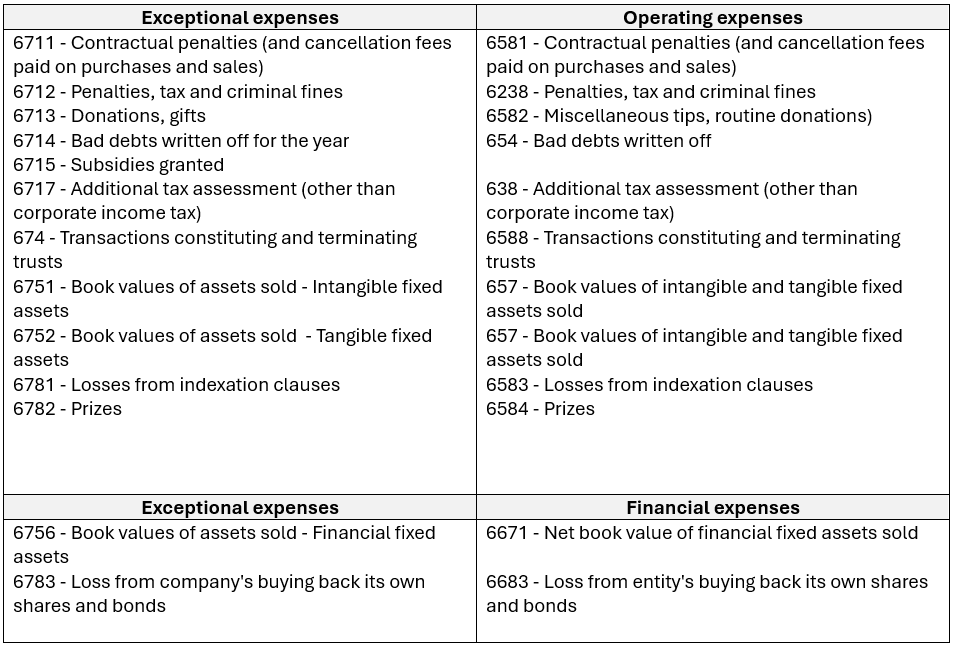

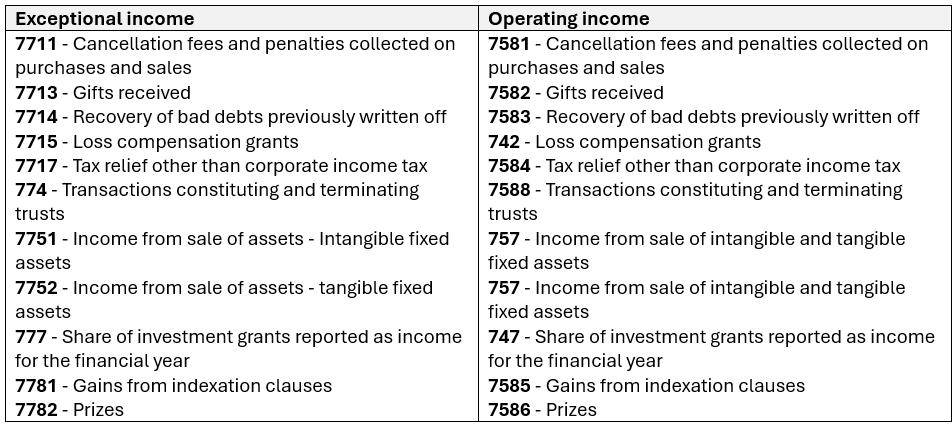

III. Modernisation of the chart of accounts and financial statements

We have created a correspondence table for the old and new charts of accounts.

To obtain a copy, please complete the form here.

Here are the main account changes for 2025:

IV. Tax implications and impacts on added value, profit-sharing, company performance bonuses and certain contractual covenants

– repercussions on information systems

- Revision of the chart of accounts

- Adaptation of some accounting rules (related to the abolition of the expense transfer technique)

- Updating of financial statements templates, the accounting manual and the closing instructions

- Configuration of reporting tool

– Tax implications concerning the calculation of the CVAE contribution and the upper limit on the CET contribution

- The Tax Law lays down an exhaustive list of the categories of accounting items that must be taken into account in the calculation of added value that serves as the base for CVAE and the upper limit of the CET.

Examples: According to tax authority practice, capital gains on the disposal of tangible and intangible fixed assets, when they relate to normal and routine activities, are counted in the base for the CVAE

Contractual penalties are excluded from the base of the CVAE.

– Potential impacts on added value calculated for profit-sharing

- An expense (or income) currently charged to exceptional items which is classified as operating income/loss under the new definition, will alter the value determined for the profit-sharing reserve (RSP).

- Employee profit-sharing = 0.5 x (net income – 5% of shareholders’ equity) x (salaries/added value).

- Added value for profit-sharing = staff costs + taxes and similar contributions + financial charges + DAP (except where included in exceptional expenses + EBT

– Potential impacts on company performance bonus agreements and other contracts:

- For example, the executives and company officers’ pay, bank covenants.

Where these are determined using an indicator based on net income/loss from operations or operating income/loss the amount of which is altered by the new definition of exceptional items.

If you have any questions, do not hesitate to contact our experts on 03.89.22.99.00